Author : Rob Temple – Sinowine

An overview of key Asian markets – showing the latest key economic indicators, import data and summary of issues facing China, the largest market in Asia, today.

Reading wine and other alcoholic drinks consumption trends in Asia is challenging at the best of times. No such undertaking should be made today without considering the economic challenges the region faces. This is particularly true in China, which has the additional complication of having import data skewed by opportunistic importers and distributors that have overstocked the market.

It’s worth taking a look at Asia’s biggest economy and the impact of current consumer confidence there before viewing the broader region.

Bottled wine imports to China peaked between 2015-2017 at around 687ML per year but have since seen a dramatic decline. Locally made wine production has also seen a rapid fall.

2024 wine imports were down to 281ML. This was up from 2023 – buoyed by a sudden inflow of Australian wines newly released from punitive tariffs. But imports continued their downward trajectory in 2025 falling to 209ML. All categories fell except Sparkling and White wines, however, values dropped 10% year-on-year vs 26% for volume.

But imports do not equate to consumption. Indeed, the extraordinary growth in wine imports that started in China 15 years ago was driven not by consumers so much as by importers and distributors, who saw wine as a more profitable alternative to the dwindling margins offered by beer and spirits. Records show that most of the newcomers to wine trading only ordered once or twice before they found a saturated market without sufficient consumption, or, that they lacked the understanding of how to manage a sensitive product.

Wine was also considered to be the new sophisticated and prestigious way to entertain in business and government circles, particularly with premium red wine brands. The impact of government curbs on entertaining – first in 2012 and more recently with even tighter controls in 2025 – gave a measurement of just how much wine went into this channel (beer and spirits categories have also been severely impacted, particularly local baijiu brands that form an essential part of formal entertainment). Restaurants are now reeling from the absence of this business and hurrying to convert their private rooms, once filled with hushed, hidden, dinners, to open-plan configurations more popular with regular diners.

Speculative importers and government-related consumption may never return to the extent they once were. This leaves us with the opportunity to understand who a consumer of wine actually is.

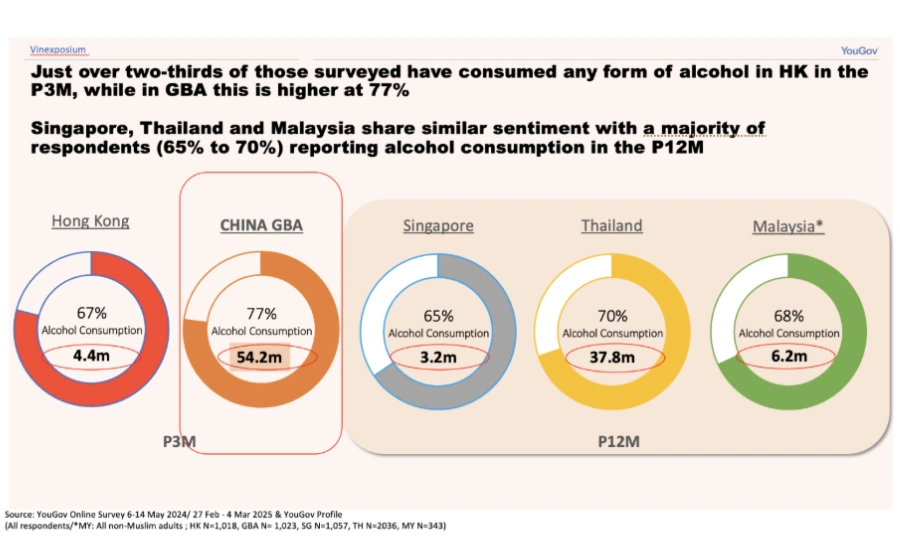

The number of genuine wine consumers in China has undoubtedly grown in recent years. A study by YouGov in 2025 measured the number of regular wine consumers (those who drink wine more than once per week) to be over 20 million in Guangdong province alone.

Credit: ©Rob Temple – Sinowine

Credit: ©Rob Temple – Sinowine

Credit: ©Rob Temple – Sinowine

But consumers today appear to be buying what they can, rather than what they want, due to the negative economic, geopolitical and demographic forces at play.

Consumer confidence is low. The Composite Consumer Confidence index is a monthly consumer survey run by the China Economic Monitoring and Analysis Centre (CEMAC) – an office of the government’s Assets Supervision and Administration Commission (SASAC). Their 0-200 point scale currently reads 89 – some way below ‘neutral’ level 100. Further evidence of reluctant spending can be seen the levels of savings of disposable income in 2025 – 34%, vs a usual 25% in recent years.

This reluctance to spend becomes more obvious when looking at current economic indicators.

It is said that China runs on three engines – foreign investment, property and infrastructure development and exports. Arguably, the first two don’t fire without export trade dollars, but all three are under significant pressure.

China’s exports to the US, the country’s largest export market, was worth US$525.7Bn in 2024. This declined more than 20% in 2025 due to US tariffs.

Nominal GDP in China is set to fall from over 27% total growth for the five years between 2019-2024 to 20% for the next 5 years. Foreign Direct Investment (FDI) in 2025 dropped for a third year running by 9.5%YOY to US$107Bn – still sizeable, but the trend shows continuing caution among investors. Local government debt has been officially published at RMB 47.5 trillion which is hindering local economic development.

These are just a few of the difficult numbers to look at. But it is declining property prices that perhaps weigh most heavily on the minds of consumers in China.

Property makes up between 20 to 30% of China’s GDP but 70% of personal assets. 90% of households in Chinese cities own their homes (vs 65% home ownership in US). Up to 20% own more than one. Property prices have fallen 20-40% from the high of 2021 when government “Three Red Lines” policy put restrictions on land sales and lending policies which popped a growing bubble in the market. UBS forecasts property prices in China will drop by 10% in 2026 and a further 5% in 2027 without strong government intervention.

Between 2008 and 2022 32% of urban residential properties sold in China were for investment purposes. In 2008 when China launched an economic stimulus package (worth some RMB4 Trillion – 12.5% of GDP at the time) to buffer the impact from the US banking crisis much of it ended up in property purchases (this alone led to a 30% growth in the real estate development in the 2010s).

But 32% more units of housing were being built each year than newly formed households. It’s no surprise that the government stepped in to cool the market in 2021.

With a population forecast to drop by 3.4% in the next 10 years and rising unemployment there is little to suggest property prices will recover soon.

This is the first time property owners have seen prices drop and this matters. Without a broadly trusted pension program property for many is a nest egg.

Several initiatives to address the downturn have already been launched by the central government (bond issuances, a “16-point plan” for property, for example). Many countries around the World are queuing up to make trade deals with China in the wake of US tariffs.

But such challenging issues will take time to resolve and in the meantime consumers will remain cautious with their spending, particularly on non-essential items. This impacts not only local business but also in hotels, bars, restaurants, shops and places of entertainment in Bangkok, Tokyo, Seoul, Taipei, Singapore, Kuala Lumpur, Hong Kong and Macau and elsewhere.

Despite the current challenges, the long-term prospects for Asia remain strong. Again, some of the data does not tell the whole story.

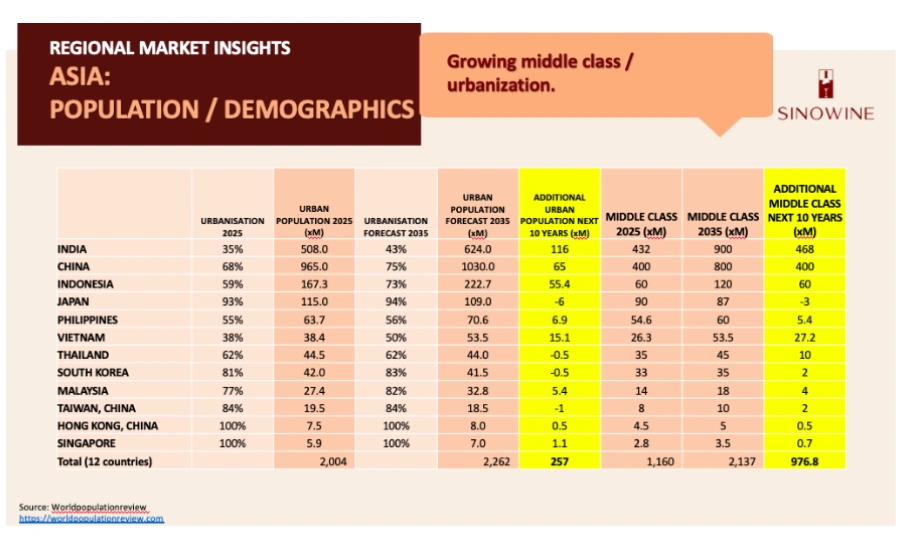

Population

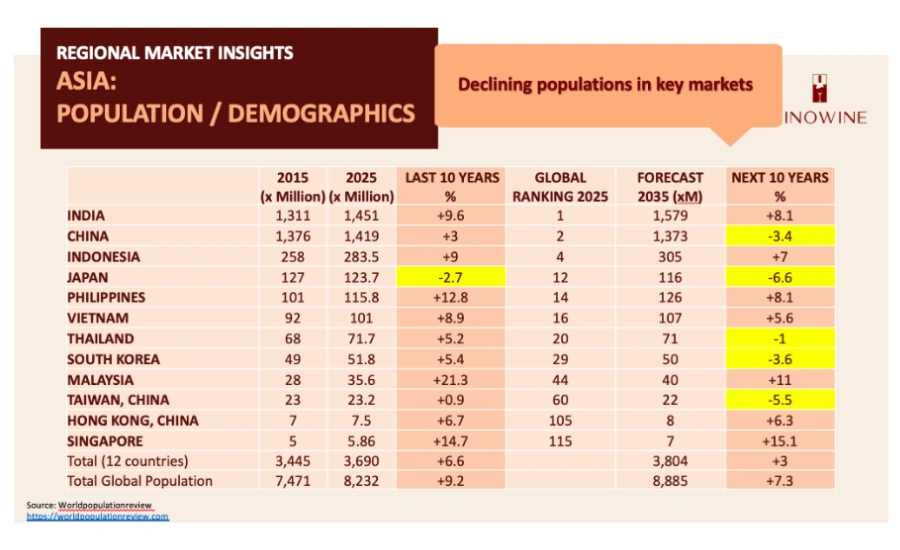

The 10-year population forecasts for the key markets in Asia vs the last 10 years show changing trends. Despite China’s projected fall in population it’s middle class is set to grow to over 800 million in the next 10 years. “Peak India” population is not likely to occur until 2060 (around 1.7 billion, according to UN reports), and a middle class that will reach 61% of the population by 2047 – that’s double the current level. South Korea, Thailand and Japan will all see their populations (and critically, their middle–class sectors) shrink over the next 10 years. We are already seeing older generations in these markets move to more premium products in the drinks arena and young consumers looking for lower alcohol / “value” drinks – a trend likely to continue over the next few years. In total, though, key Asian markets are forecast to add over 250 million people to city populations in the next decade as urbanisation grows.

Credit: ©Rob Temple – Sinowine

Credit: ©Rob Temple – Sinowine

Credit: ©Rob Temple – Sinowine

Credit: ©Rob Temple – Sinowine

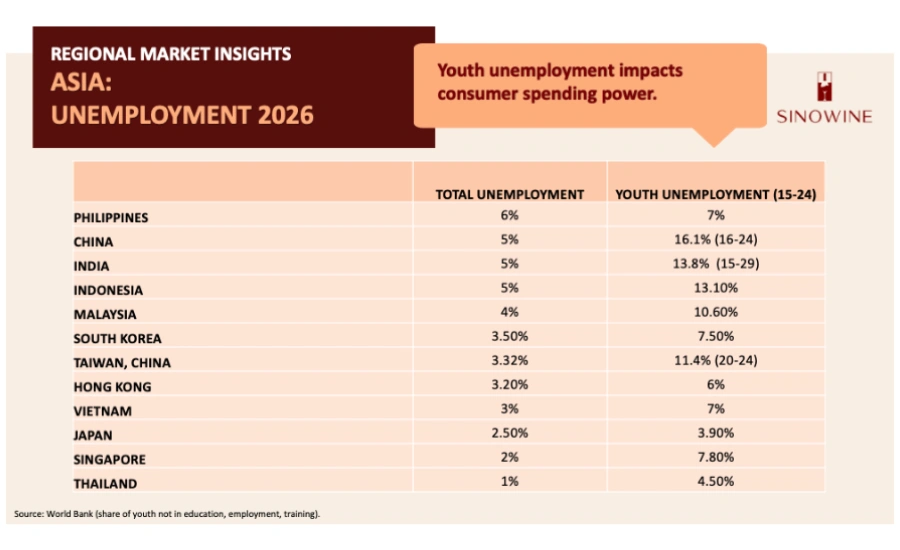

Youth Unemployment

Much has been written about the habits and concerns of Gen Z group and while there is little doubt their thoughts differ from older generations when it comes to consuming alcohol, affordability must be part of their consideration, particularly those without a job. Unemployment of under-25s in China officially now stands at 16.1%, but those who do have a job may not feel secure in that employment or may have a low starting salary.

Credit : ©Rob Temple – Sinowine

Credit : ©Rob Temple – Sinowine

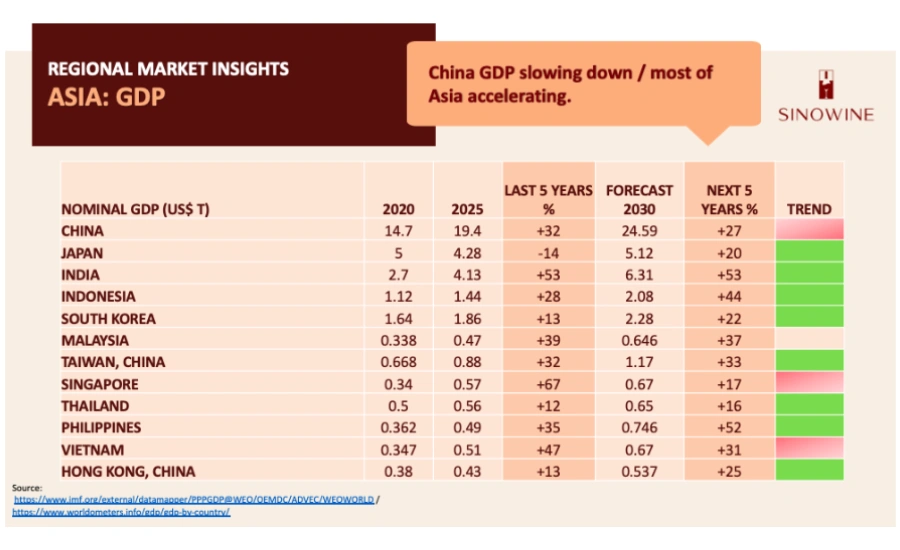

GDP

Until recently, the IMF forecasted GDP growth to accelerate in the coming years. The threat of long-term high oil prices has forced a rethink. Still, Asia will record higher growth rates than much of the rest of the World.

As the World scrambles for trade deals with China in the face of US tariffs, we may see an improvement in current forecasts there. Early signs for 2026 are positive.

Japan’s prime minister Sanae Takaichi promises to turn around an ailing economy there through investments in tech industries in particular. A stubbornly weak Yen is making life hard for importers of foreign products, including wine and spirits.

South Korea has a similar plan and is injecting a huge budget into tech to raise its economy. Taiwan is ahead of both in the technology field and is on the cusp of a massive wave of demand for its chips that power much of the growing AI industry.

Credit: ©Rob Temple – Sinowine

Credit: ©Rob Temple – Sinowine

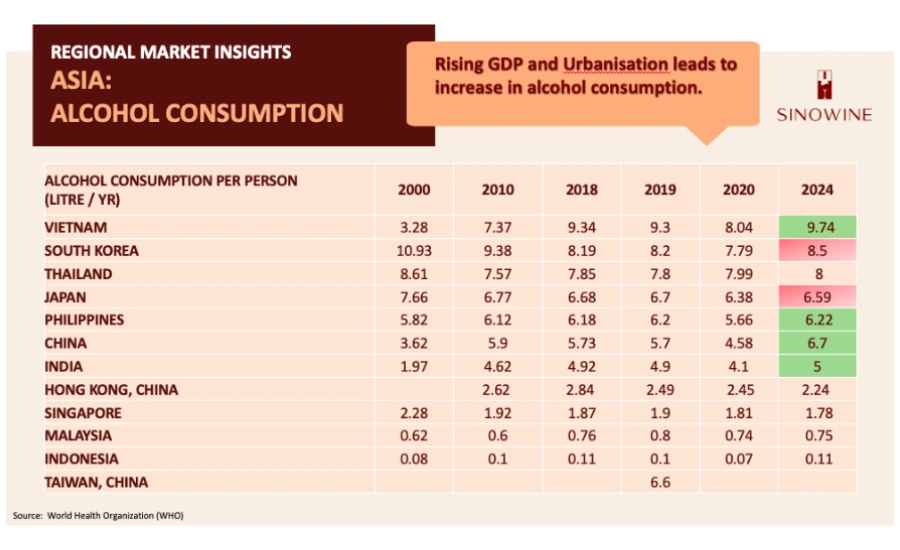

Alcohol Consumption

This brings us to the topic of alcohol consumption. Wealthier, urbanised populations enjoying convenient city living and disposable incomes have increasing access to sophisticated retail and F&B outlets.

The Vietnamese are the largest per capita consumers of alcohol in Asia today and drink three times as much as they did in 2000. 91% of it is beer, 8% spirits, and around 1% wine – but with urbanisation at 38% this mix is not surprising.

On the other end of the scale, Japan’s aging population (30% of Japanese are over the age of 65, and Japan shrinks by 96 people per hour) has already changed its drinking habits to higher average spend and lower volume consumption. Young consumers have not taken up the national drink sake, instead, preferring beer and wine, and increasingly, whisky (there are now 500 producers of whisky in Japan). Sake, though, has growing appeal overseas with export values doubling in the last 5 years to 46BN Yen in 2025.

Credit: ©Rob Temple – Sinowine

Credit: ©Rob Temple – Sinowine

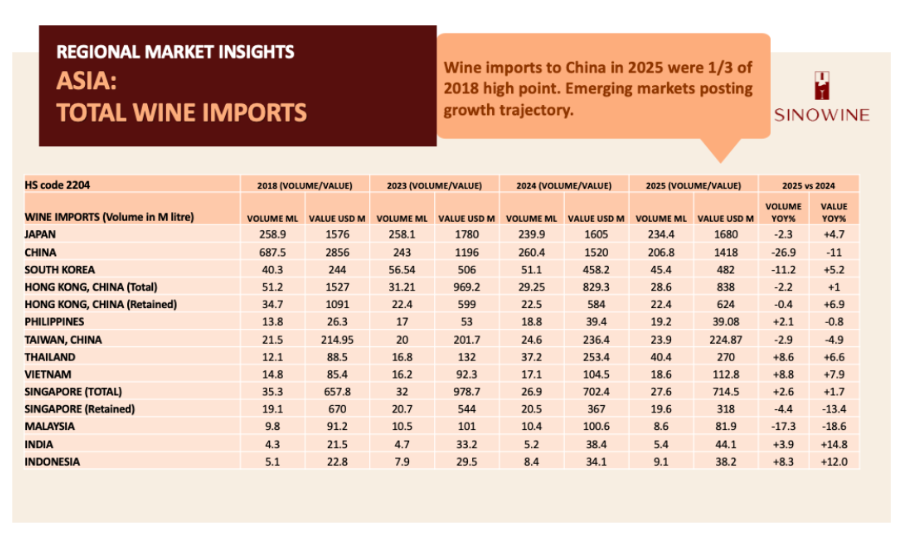

Wine Imports

We have already covered the reasons for China’s sudden spike in imports and recent declines. It is worth noting where wine sits in the alcohol landscape. Around 49% of the alcohol category by value is beer, and about the same percentage for spirits (95% of spirits are local baijiu products), leaving around 2% for wine (of which half is bottled locally). As with all markets, wine brands struggle to compete with advertising and promotion dollars that beer and spirits brands enjoy.

Despite the small market share, wine occupies a substantial space in supermarket drinks sections. Recently, key supermarket operators in China have vastly improved the quality, price, and presentation of their wine portfolios. This has led to a new level of trust from consumers. “Instant retail” is becoming the norm – a bottle of chilled wine can be delivered to a home, or, crucially, to a consumer in a restaurant, within 25 minutes. This opens a vast opportunity to wine in the on-trade where outside of tier one cities wine can be hard to find.

Another encouraging observation seen across all channels in China is the uptick in white wine consumption. Consumers of white wines are the most likely to drink on taste (unlike for red wine, which may be consumed for image or be given as a “premium” gift). This shows a level of maturity that bodes well for the future of wine.

India is growing from a small base (less than 1% of total alcohol consumption value) due to the complexities of local supply chains and strong spirits and beer culture. India’s local wine production commands around 70% of the total wine market. Australia currently takes about 40% market share of imports by volume (mostly TWE and AWL and due to the Australia-India Economic Cooperation and Trade Agreement) but a new Free Trade Agreement with EU will cut import taxes from 150% to 20-30% for wine (reductions from 150% to 40% for spirits and 110% to 50% for beer) will see a levelling of the playing field.

Crédit : ©Rob Temple – Sinowine

Crédit : ©Rob Temple – Sinowine

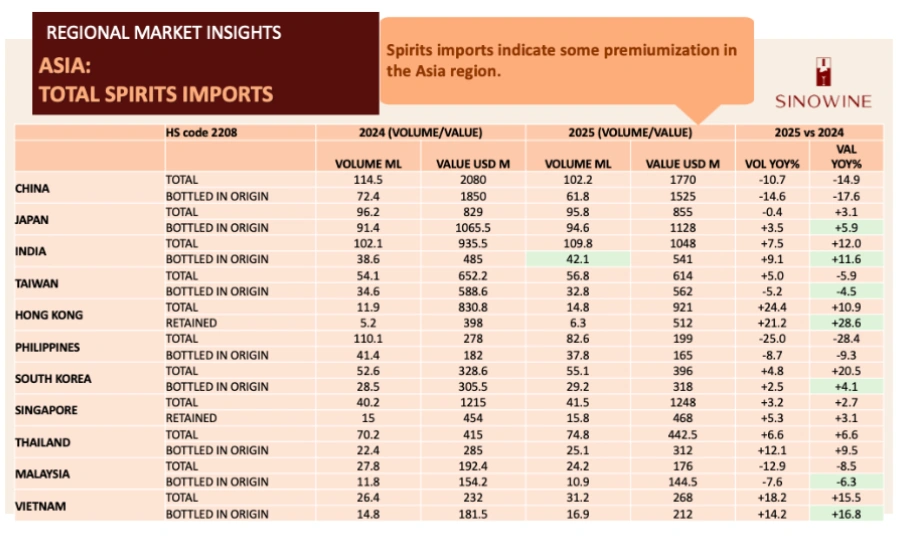

Spirits Imports

Weak consumer sentiment and a challenging tourism industry have dented spirits consumption in Thailand, particularly of premium brands. Strong cocktail growth has been beneficial to low-priced and white spirits here and across Asia. Generally, though, there are signs of trading up in emerging markets and traditional markets. Cocktail bars are springing up across China. Bar owners can make up to five times higher margins with spirits-based drinks than with wine. Canned RTD drinks are more convenient for consumers and retailers than standard glass bottles of wine.

Credit : ©Rob Temple – Sinowine

Credit : ©Rob Temple – Sinowine

Ultimately, Asia is a region of great diversity. Growing GDP and urbanisation across most of the region will drive consumption. Higher incomes in expanding cities will outweigh the short-term economic challenges. It’s not yet possible to be sure how rapidly emerging AI technology will impact Asia (analysts predict mass job displacements and mass job creation – either way, an upheaval in job markets seems inevitable). Engaging with the consumer in their language, linguistically and culturally, will be as important as ever for brand owners to benefit from this rapidly evolving continent.

About Rob Temple

Rob Temple has over 30 years of experience in building wines and spirits distribution companies, mostly based in Hong Kong and Greater China. His Hong Kong-based company, Sinowine Ltd. represents premium wines and spirits brands in the Asia markets, working with importers, distributors, retailers, airlines and duty-free operators and offering a range of business development services.